Corporate Overview

- A Diversified Business Portfolio

- Key Performance

- Strategy Drives Positivity

- Positvity Steers Performance

Statutory Reports

Key Business Highlights

DOWNLOAD CENTER

Management Discussion

and Analysis

The Sugar Industry

As one of the largest agro-based industries in India, with a total turnover of over ₹1,00,000 crore, the Sugar industry, which includes sugar and its co-products, contributes significantly to the nation’s socio-economic development.

In the Sugar Season (SS) 2018-19 (October to September), around 732 mills produced more than 33 million tonnes of sugar, making India the world’s largest sugar producer. India also maintained its leadership position as the world’s largest consumer. The industry’s value chain encompasses around 50 million farmers, along with around 2.5 million farm and industrial workers who are involved in sugarcane farming and the sugar manufacturing value chain.

Having emerged as a major driver of the country’s progress, the Sugar industry continues to be central to the Government of India’s strategic focus. The Government’s proactive interventions have been crucial for the industry, which faces tremendous challenges due to excess production and carryover stock. The Government reforms have, in fact, been critical to the success of the sugar companies in recent years.

Among the key policy interventions of the Government are the creation of buffer stock, provision of soft loans, establishment of Minimum Selling Price (MSP) with a controlled monthly release mechanism for the sale of sugar, and the introduction of a financially supported export programme. These interventions have helped the country in maintaining the demand-supply balance for the Sugar industry, while securing the livelihood of farmers and ensuring that sugar companies do not face financial stress.

Further supporting the supply side management of the Sugar industry is the lower quantum of sugar production achieved as a result of the Government’s thrust on ethanol production. Prompt approval of projects related to ethanol capacity enhancement assisted the diversification of the industry and the diversion of surplus sugarcane juice/syrup and B-heavy molasses towards the production of ethanol during the year.

The expansion of the global sugar deficit was also a positive factor in raising global sugar prices, resulting mainly from lower sugar production in Brazil and Thailand, thus leading to supply side shocks. This has further augmented the Indian sugar industry’s export programme.

THE SUGAR MARKET

As a major propeller of India’s progressive agenda, the Indian sugar industry has emerged as a key driver for the nation’s rural economic development. A decade of concerted sugarcane development and adoption of more scientific agronomical practices, together with timely regulatory changes, has led to significant transformation in the Indian sugar industry over the year. It has positioned India as a leading producer of sugar in the world.

Furthermore, the extensive sugarcane development programme undertaken by the industry has helped farmers to not only increase their yields but also double their incomes. Mechanisation of sugarcane farming, introduction and propagation of early maturing and high sucrose sugarcane varieties, adoption of the latest scientific techniques of farming, inter-cropping (the ability to plant two crops at a time) etc. have strengthened the financial robustness of sugarcane farming in the country. However, the sector is still impacted by weather conditions, such as the vagaries of the monsoon.

During SS 2019-20, sugarcane area, as reported by the Agriculture Department, was 52.45 lakh hectares, down by 5.51% year-on-year. The major drop was accounted by the states of Maharashtra and Karnataka, which were adversely impacted by poor water availability in the plantation period and floods during the crucial growth stage.

As on March 31, 2020, the country’s sugar output for SS 2019-20 stood at 23.3 million tonnes, down by 6.4 million tonnes year-on-year. COVID-19 has impacted the sugar production positively, as gur (jaggery) and khandsari (unprocessed sugar) manufacturers shut down operations in UP early because of the lockdown, which led to the diversion of an additional quantity of sugarcane to mills for crushing. The sugar production in the country, till May 31, 2020, stood at 26.82 million tonnes, and is estimated to be over 27 million tonnes in SS 2019-20. This decline in production is a result of reduced output from Maharashtra and Karnataka, as well as the diversion of B-Heavy molasses towards ethanol production, which resulted in lower sugar output by around 0.5 million tonnes. The diversion during this season was twice the quantity diverted during the previous season.

The sugar production in the country, till May 31, 2020, stood at 26.82 million tonnes, and is estimated to be over 27 million tonnes in SS 2019-20.

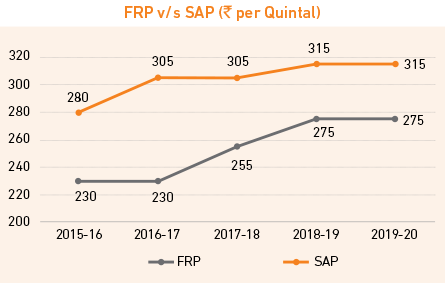

The Central Government announced Fair and Remunerative Price (FRP) for sugarcane for SS 2019-20 at ₹2,750 per tonne - unchanged from the previous year, as per the recommendations of the Commission for Agricultural Costs and Prices (CACP). The UP Government also retained the State Advised Price (SAP) at the level of the previous sugar season, at ₹3,150 per tonne for normal varieties delivered at factory gate, with a premium for early maturing varieties and a discount for sugarcane delivered at out centres as well as for rejected varieties.

The high cost of sugarcane, and resultant higher cost of production of sugar, makes it difficult for Indian manufacturers to compete in the international market, and adversely affects the sugar exports programme. Under the circumstances, exports are viable only with Export subsidy or financial assistance from the Government. Sugarcane price in India is 60-70% higher than that of Brazil or Thailand.

As per the Food Ministry’s data, as on May 28, 2020, sugarcane arrears in sugar season 2019-20 stood at ₹17,134 crore on FRP basis and ₹21,238 crore on SAP basis. Sugar prices remained range bound, and in most parts of the country remained just above the MSP, thereby impacting the capability of the mills to pay sugarcane farmers. CACP, in its recommendations to the Government for the fixation of FRP, has strongly recommended implementation of the Revenue Sharing Formula (RSF) based on revenue generated from sugar and primary co-products, as earlier recommended by the Dr. Rangarajan Committee. Adoption of the formula by all States is the key to long-term sustainability of the Sugar sector. During the period when RSF is lower than FRP, the difference can be paid to the farmers through a Price Stabilisation Fund (PSF), which can be created by imposing tax on soft drinks / beverages, as well as dual pricing for industrial and household sectors, that can be planned to generate extra funds and keep those under PSF. The Commission recommended setting up of a Committee to explore various possibilities for managing the PSF.

CACP also recommended the abolition of SAP and adoption of FRP uniformly, throughout the country. In case the State Governments still decide to announce SAP, the difference between FRP and SAP should be directly paid by the State Government to the farmers.

While the Government has supported the industry with soft loans, benefits of MSP, buffer stocks, export subsidies and incentives, the root cause - mismatch between sugarcane price and sugar price - has remained unresolved. In order to bring financial stability to the Sugar industry, key reform for linking sugarcane price with sugar price is essential.

Domestic

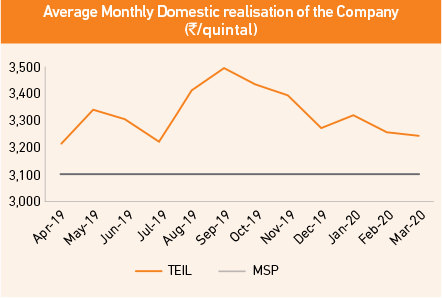

The average sugar price trend showed volatility during FY 20, with a peak of ₹3,490 per quintal in September 2019 from a bottom of ₹3,210 per quintal in July 2019. The variation in the domestic sugar prices was primarily due to difference in the monthly release of sugar for sale between various states of the country. Sugar price realisation for Triveni has always been much above the Minimum Selling Price (MSP) announced by the Government.

Domestic price is more fundamentally driven by the quota system, with the Government determining the quantity to be supplied in a month. This is done through monthly despatch quota prescribed for each sugar mill, taking into consideration the consumption pattern. It allows the Government to regulate the prices subject to MSP. The consumer demand in India is almost consistent but institutional supplies are based on seasonal factors and festivities.

From the above graph, it can be seen that a dip in sugar prices was followed by a rise in price levels and vice versa. This was due to the checks by Department of Food and Public Distribution (DFPD) with regard to liquidation of stocks and imposition of balanced monthly despatch quota for each sugar factory. Throughout the year, this variation in prices also helped in keeping under check the speculative stocks positioning by Institutional buyers and the volume of sugar inventory in transit. A few deficit states, like Andhra Pradesh, Telangana and Tamil Nadu, were well catered by supplies from the Western states of India, whereas majority of Gujarat and Rajasthan markets were covered by the North Indian mills.

Due to the lockdown imposed by the Central Government from the last week of March 2020, sugar prices have fallen to the level of Minimum Selling Price (MSP) of ₹31 per kilo from ₹32.5 per kilo in February 2020. The sugar mills were unable to fulfil their monthly sales quota allocated by the Government due to the significantly lower institutional demand in this period. The drop in sales consequently led to pressure on the working capital requirements of sugar mills, which further negatively impacted the sugarcane payment to farmers.

Global

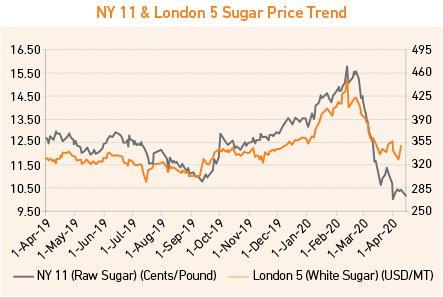

International price contracts of both raw and white sugar traded mostly based on Thailand and Brazil production estimates. After a peak of 15.78 USD cents/pound, the near-month contract of raw sugar dipped to 10 USD cents/pound.

Likewise, white sugar plunged to USD 294 per tonne after touching a peak of USD 451 per tonne.

The most challenging part of the Surplus to Deficit price trend was the transitional changes in the fundamentals, in addition to some other factors like drastic price decline against short of large specs, China’s slow buying, Indian export subsidies etc. Thailand’s varying crop estimates, El Niño effects and regional carry forwards also triggered fluctuations. Thus, both raw and white sugar prices have been under pressure – because of global oversupply on the one hand and ramping up of India’s exports on the other. White sugar’s premium also varied during the timeframe - from a bottom as low as USD 40. During the last fortnight of March 2020, the near-month contract was additionally under undue pressure due to COVID-19.

The Brazilian currency traded at an all-time low and oil prices also remained weak during April-May 2020. Owing to the demand destruction of sugar and fall in ethanol prices, Brazil Real came down drastically. The impact of COVID-19 resulted in lower sugar demand, stalled exports, and lower ethanol sales. The world also witnessed sharp decline in oil prices due to COVID-19 and various geopolitical factors. This impacted the mix of sugarcane usage in Brazil for manufacturing of ethanol vis-à-vis sugar, while in Thailand sugar production declined due to drought. With shortage of packing materials and labour at ports, there were problems in shipping sugar consignments to export markets. This resulted in decline in the global sugar prices. Lower demand adversely impacted the sale of both sugar and ethanol, with maintenance of sugar inventory and storage of ethanol emerging as major problems for integrated sugar manufacturers.

The world also witnessed sharp decline in oil prices due to COVID-19 and various geopolitical factors. This impacted the mix of sugarcane usage in Brazil for manufacturing of ethanol vis-à-vis sugar, while in Thailand sugar production declined due to drought.

The Government derives its power from the Essential Commodities (EC) Act 1955, which gives it the authority to declare policies such as the monthly sales quota mechanism for individual sugar factories, the minimum selling price for sugar (MSP), the creation of a sugar buffer stock, among others. Sugar has been declared an essential commodity as it is an item of mass consumption, with sugarcane being a highly remunerative crop that attracts and supports millions of farmers and their families across the country. The controls with respect to sugar include determining the mill-wise monthly despatch quota to maintain sugar prices, subject to MSP, in order to meet consumption demand. Other controls relate to managing a buffer between the deficit and surplus states, creating buffer stocks to mitigate higher sugar inventories, export decisions to correct surplus sugar inventory, and also to provide soft loans in challenging conditions to pay the sugarcane price. The controls with respect to sugarcane are fixed as per FRP by the Central Government and in some states, including Uttar Pradesh, the State Advised Price (SAP) is fixed by the State Government. Further, the Government of India has taken several steps to increase the viability of the industry through optimum utilisation of the co-products and to encourage several streams of revenue for the sugar mills.

Typically, large inventories of sugar would have had a devastating impact on pricing, but introduction of the MSP by the Government has prevented such a collapse. It is still argued by the industry association, however, that the MSP is lower than the average cost of production of the country. MSP offers a base price and, for most parts of the country, the sugar realisations are close to MSP, whereas the average realisation for UP sugar mills for sale of crystal sugar are typically higher than MSP, with refined sugar fetching some premium to the crystal sugar. The introduction of Maximum Admissible Export Quota (MAEQ), and the subsidy linked to it, encouraged the noncoastal sugar producing states of India to actively participate in the export programme. Various initiatives were also taken to engage in bilateral talks with nearby countries to promote the export of sugar from India.

In order to maintain the demand-supply balance in the country, the Government took various timely decisions during the fiscal under review:

- The Cabinet Committee on Economic Affairs (CCEA) approved creation of buffer stock of 4.0 million tonnes of sugar for one year - from August 1, 2019 to July 31, 2020, which would incur estimated maximum expenditure of ₹1,674 crore. The reimbursement under the scheme would be met through quarterly payments to sugar mills, to be directly credited into the farmers’ account on behalf of the mills against sugarcane price dues.

- MAEQ - An Export Quota of 6.0 million tonnes was allocated to all sugar mills on September 12, 2019, with export date till September 30, 2020. The Government notified a scheme for providing Export subsidy of ₹10,448 per tonne for export of sugar, covering expense on marketing cost, including handling, upgrading and other processing costs as well as costs of international and internal transport and freight charges on export of sugar. All such assistance under the scheme will be used to clear sugarcane payment dues of farmers.

- On July 24, 2019, the GoI announced FRP of ₹2,750 per tonne for sugarcane to be purchased in SS 2019-20 – the same level as in SS 2018-19, corresponding to 10% recovery with a premium of ₹2.75 per quintal for every 0.1% rise in recovery.

Domestic

Indian Sugar Industry

The Government of India has fixed an export target of 6.0 million tonnes for SS 2019-20. However, it is expected that the likely export of sugar will be in the range of ~5.0 million tonnes, on account of the impact of COVID-19, volatility in global sugar prices etc. Port activities also slowed down amid the COVID-19, thus impacting exports. Concurrently, international sugar prices plummeted to their lowest levels in recent years, though a few exports did continue to some destinations, based on specific demand. Mills had contracted about 4.2 million tonnes of exports by the beginning of May, and exports are likely to resume in the coming months of 2020. As per the industry association, “with demand picking up, and an expected increase in demand to refill the pipeline, which will come sooner or later, sugar sales in the 2019-20 sugar season ending September may be around 0.5 million tonnes less than last year”. This will reduce the annual estimated consumption to about 25 million tonnes, and as a result, the estimated sugar inventory as at the end of September 2020 would be approximately 11.5 million tonnes.

With the re-opening of the country, especially markets, malls and restaurants, in the coming days, sugar demand should rise and reach its normal levels, thus translating into better sales. However, the recovery from COVID-19 related price falls will be slow, as consumption will remain subdued and global output is also estimated to rise.

With preliminary estimates of SS 2020-21 in the range of 31 to 32 million tonnes, India is expected to face another bumper year of sugar production, where industry will need to divert substantially more sugar towards ethanol production and also actively participate in the export campaign with support from the Government.

The Government of India has fixed an export target of 6.0 million tonnes for SS 2019-20. However, it is expected that the likely export of sugar will be in the range of ~5.0 million tonnes

Global

Sugarcane crushing in the Centre South Brazil (CS) ended at 589.90 million tonnes for the 2019-20 (April-March) season, which is an increase of 2.9% from 573.17 million tonnes a year ago. In the last 22 years, this season recorded the lowest recovery and only 34.32% sugarcane was used for sugar production, with the balance 65% of sugarcane used for manufacture of ethanol. The sugar production was marginally higher by ~1% at 26.73 million tonnes as compared to the previous season.

Thailand crushed 74.89 million tonnes of sugarcane in the 2019-20 season that ended in April, and produced only 8.27 million tonnes of sugar. The ongoing drought since last year has impacted the yield per plantation, which, along with low domestic sugarcane prices, led farmers to turn to other crops.

The world sugar balance is in deficit for the 2019-20 season, mainly due to supply side shocks resulting from decline in sugar production in the key sugar producing countries of Brazil, India and Thailand.

THE ETHANOL MARKET

The Central Government has been actively promoting the production and blending of fuel ethanol with petrol, and has targeted 10% blending (EBP10). Apart from being environment-friendly, ethanol also ensures fuel security for the country, conserves foreign exchange, and creates an additional revenue stream for the sugar industry to minimise the impact of its inherent cyclicality.

While the target is 10% blending, the country has achieved about 5% blending last year under the Ethanol Blending Programme (EBP) which helped in reducing dependence on oil and lowering pollution while saving ₹6,000 crore in foreign exchange annually.

With population growth and increasing urbanisation pushing the need for mobility, India’s transportation sector is growing rapidly, causing dependence on oil to also concurrently rise. Considering the burgeoning oil import bill and the growing concern for the environment, there is need to adopt non-conventional fuels. While the target is 10% blending, the country had achieved about 5% blending last year under the Ethanol Blending Programme (EBP), which helped in reducing dependence on oil and lowering pollution, while saving ₹6,000 crore in foreign exchange annually. Ethanol has about 30% oxygen, which in turn enables fossil fuel to burn much better within the engine, thus significantly reducing the emissions. Ethanol, being a value-added product from molasses - a coproduct in the manufacture of sugar from sugarcane - benefits sugarcane farmers across the country.

The key drivers for the Ethanol Industry are:

The Government is proactively promoting the setting up of distillation capacities for the manufacture of ethanol for blending with petrol by offering substantial subvention of interest on loans required to set up distilleries, and has fixed remunerative ethanol prices through Oil Marketing Companies (OMCs). Higher ethanol prices have been fixed for ethanol manufactured from B-heavy molasses and directly from sugarcane juice, to encourage higher volume production of ethanol. As per industry estimates, on an average, B-Heavy molasses diverted by the Sugar industry during SS 2019-20 will be equivalent to at least 0.5 million tonnes of sugar.

For the marketing year (December–November) 2019-20, Oil Marketing Companies invited bids for 511 crore litres of ethanol, against which the quantity offered in the first round is approx. 163 crore litres, of which LOIs for 156.5 crore litres have been issued. Further, in January 2020, OMCs tendered additional 253 crore litres. The drastic reduction in bids is mainly attributable to lower sugarcane production in the major ethanol producing states of Maharashtra and Karnataka. The situation was further aggravated by the UP Government’s decision to increase the reservation of molasses from 16% last year to 18%, and to extend this reservation to captive consumption of molasses, which was not there last year.

The OMCs, on June 1, 2020, floated the third round of Expression of Interest (EoI) submission, inviting bids from ethanol producers for another 990 million litres of ethanol for supplies during July-November 2020.

Historical information on the ethanol requirement, contracts finalised and supplied by sugar companies since 2014-15 is as under:

Marketing Year for ethanol supplies (December - November)

(*) up to May 4, 2020

The various policy initiatives undertaken by the Indian Government for ethanol blending, over the years, include:

A notable intervention by the Government in this area has been the National Biofuel Policy, announced in 2018 for accelerated development and utilisation of biofuels in view of the current direct and indirect subsidies to fossil fuels and distortions in energy pricing.

The Policy categorises biofuels as:

- “Basic Biofuels” - First Generation (1G) bioethanol and biodiesel

- “Advanced Biofuels” - Second Generation (2G) ethanol, Municipal Solid Waste (MSW) to drop-in fuels

- Third Generation (3G) Biofuels, Bio-CNG etc.

The Policy expands the scope of raw material for ethanol production by allowing use of sugarcane juice, sugar containing materials like sugar beet, sweet sorghum, starch containing materials like corn, cassava, as well as damaged foodgrains like wheat, broken rice, rotten potatoes that are unfit for human consumption, for ethanol production.

The Government has fixed higher price for ethanol derived from different raw materials under the EBP, for ethanol supply from December 1, 2019 to November 30, 2020, as under:

- The price of ethanol from C-heavy molasses route increased from ₹43.46 per litre to ₹43.75 per litre

- The price of ethanol from B-heavy molasses route increased from ₹52.43 per litre to ₹54.27 per litre

- The price of ethanol from sugarcane juice/sugar/sugar syrup route fixed at ₹59.48 per litre

- Additionally, GST and transportation charges will also be payable, and OMCs have been advised to fix realistic transportation charges so that long-distance transportation of ethanol is not disincentivised

In order to boost the country’s ethanol production, the Government has approved 362 projects with an investment of ₹18,600 crore for enhancing additional ethanol production capacity of 400 crore litres in the next two years. The total ethanol production capacity would touch 755 crore litres, which will help the country achieve 20% ethanol blending with petrol, by 2030. The Government is proactively pushing to augment ethanol production capacities in order to achieve successful 10% ethanol blending by 2022 and 20% by 2030.

During the year, the Ministry of Environment also announced waiver of green clearance requirements for distilleries that are planning to produce up to 50% more ethanol than their nameplate capacity without increasing pollution, which will help sugar mills to divert more molasses towards ethanol.

THE CO-GENERATION MARKET

Co-generation is a decentralised incremental power addition that has many associated benefits, such as mitigated risk of loss of power to large areas due to shut-down, reduced transmission and distribution losses, sustained local power supply, and employment generation. The importance of having high efficiency grid connected co-generation power plants for generating exportable surplus has been well established in the Indian sugar mills.

The installed power generation capacity in India was 3,70,106 MW as on March 31, 2020, of which 87,028 MW was renewable power.

The installed power generation capacity in India was 3,70,106 MW as on March 31, 2020, of which 87,028 MW was renewable power. The Government has set a target of 175 GW renewable power installed capacity by the end of 2022, which includes 60 GW from wind power, 100 GW from solar power, 10 GW from biomass power and 5 GW from small hydropower. The all-India potential of bagasse-based co-generation is estimated at 7,000-7,500 MW. UP is the leading state in bagasse-based power generation, with an installed capacity of around 1,200 MW. The potential of bagasse co-generation within UP is around 1,500 MW from over 130 sugar mills.

India has witnessed sharp increase in energy consumption, triggered by high levels of economic growth and industrialisation, in the past couple of decades. Power demand in the residential sector has also increased. However, limited fossil fuel availability necessitates utilisation of non-conventional fuel sources for power generation. Bagasse co-generation not only reduces dependence on conventional fuel sources but also helps in saving precious foreign exchange by limiting the import of coal. The clean energy so generated with bagasse has a favourable impact on climate. India’s climate action plan aims for 40% installed capacity from non-fossil fuel by 2030. Using bagasse for power generation also leads to significant revenue generation for sugar mills through the sale of electricity.

Demand-Supply Scenario

The potential for bagasse co-generation lies mainly in the country’s nine key sugar-producing states, especially U.P., since it is one of the highest sugarcane-producing states. Lately, due to availability of cheaper power, there has been reluctance on the part of UPPCL to purchase bagasse-based co-generation power. The rates for bagasse-based co-generation power have thus been revised downwards by the Regulator, Uttar Pradesh Electricity Regulatory Commission (UPERC) effective from April 1, 2019.

2020 Triveni Engineering, All Rights Reserved

Design & Developed by RDX Digital Pvt. Ltd.